You don’t lose wealth in one big blow. You lose it $47 at a time — through four invisible drains most high-earning Australian couples never think to check.

BY VICTOR IDOKO, CFA, CFP, M.COM (FINANCE) · FOUNDER, CFV ADVISORY

Here’s a paradox that plays out in households across Sydney, Melbourne, and Brisbane every week: a couple earns $280,000 combined. They own a home, they save something each month, and they take a decent holiday once a year. By any reasonable measure, they’re doing well.

And yet — the wealth they expect to be building feels somehow behind where it should be. The savings account grows slowly. The mortgage barely shifts. The super balance feels unremarkable for their age.

In most cases, they’re doing nothing dramatically wrong. They’re just leaking.

Wealth doesn’t disappear in a single catastrophic event. It seeps out through small, recurring drains that compound silently — year after year — not because of poor decisions, but because no one has ever laid everything out and looked at the whole picture together.

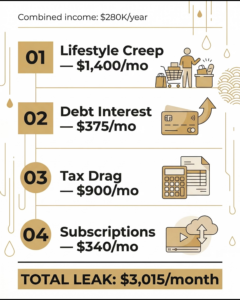

WHERE YOUR HOUSEHOLD INCOME QUIETLY DISAPPEARS

|

COMBINED HOUSEHOLD INCOME $280,000 per year |

▼

01 Lifestyle Creep$1,400/mo |

02 Debit Interest $375/mo |

03 Tax Drag $900/mo |

04 Subscriptions $340/mo |

| TOTAL MONTHLY LEAKAGE: $3,015 / month (≈ $36,180 per year) |

| “Two incomes, a good lifestyle, and somehow never quite getting ahead. Sound familiar? You’re not imagining it — and you’re certainly not alone.” |

THE FOUR LEAKS — IN DETAIL

| 01 |

Lifestyle Creep: The Leak You Don’t Notice Until You Look Back ↓ AVG. DRAIN: $800 – $2,400 / MONTH When income rises, spending rises to meet it — almost automatically. The slightly nicer suburb. The car upgrade. The restaurant meals that replaced home cooking when both partners got busier. Each decision made sense at the time. The problem isn’t the spending itself. It’s that lifestyle costs permanently embed themselves into a budget, while the income that funded them can fluctuate. By the time couples realise their lifestyle costs have quietly grown by $1,500 per month compared to three years ago, those costs feel non-negotiable. A real pattern we see: A couple on $320K earns $40K more than they did in 2021. Their savings rate hasn’t moved. Their lifestyle absorbed every dollar of the increase — and they couldn’t tell you exactly where it went. |

| 02 |

Debt Interest: Paying the Bank to Tread Water ↓ AVG. DRAIN: $400 – $1,800 / MONTH Australia’s interest rate environment has shifted significantly. Couples who locked in historically low rates in 2020–2021 and haven’t revisited their mortgage are often sitting on a rate that’s no longer competitive. Beyond the mortgage, personal loans, car finance, and buy-now-pay-later balances each carry their own interest drag. Most couples have never added up the total monthly interest they’re paying across all debt simultaneously. Typical example: $850K mortgage at 6.7% vs. a negotiated rate of 6.19% = $357/month in unnecessary interest. Over 5 years: $21,420 straight to the bank instead of your offset account. |

| 03 |

Tax Drag: Paying More Than the Law Requires ↓ AVG. DRAIN: $500 – $3,000+ / MONTH The Australian tax system rewards structure — but only if you’ve taken the time to build it. For dual-income couples with combined earnings above $180,000, there are typically meaningful opportunities in salary sacrifice, super contributions, investment structure, and income splitting that go completely untouched. This isn’t aggressive tax minimisation. It’s simply using the system as it was designed. But it requires someone to look at both partners’ income, investments, and goals — and build a structure accordingly. Common gap: Partner A earns $180K. Partner B earns $95K. Neither has optimised super contributions. With the right strategy, this couple could reduce their combined tax bill by $8,000–$14,000 per year — legally, straightforwardly, and immediately. |

| 04 |

The Subscription & Insurance Overlap Problem ↓ AVG. DRAIN: $150 – $600 / MONTH This is the leak that surprises people most, because it doesn’t feel financial — it feels administrative. Streaming services that stack up. Gym memberships used twice a year. Phone plans paying for data that isn’t needed. Dual-income households often carry duplicated insurance cover without realising it. Life insurance through super for both partners, plus a separate policy. Income protection that overlaps. Private health with extras neither partner claims. Real finding from a client review: A couple was paying for life insurance inside super and through a standalone policy — with $1.2M of overlap. They were spending $340/month for cover they’d already bought. |

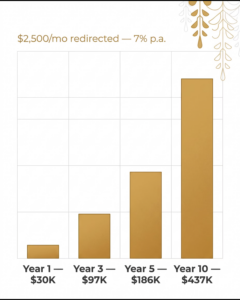

WHAT $2,500/MONTH REDIRECTED BUILDS OVER TIME

Assumes 7% p.a. compounding. Illustrative only.

| $30K

█ Year 1 |

$97K

█ Year 3 |

$186K

███ Year 5 |

$437K

████████ Year 10 |

|

$36,180 AVERAGE ANNUAL LEAKAGE IN DUAL-INCOME AUSTRALIAN HOUSEHOLDS Not lost to a bad investment. Not blown on something indulgent. Quietly drained through structure problems most families never knew existed — and never went looking for. |

The important thing to understand is that none of these leaks require a dramatic lifestyle change to fix. You don’t need to cancel everything, downsize your home, or live frugally. You need to find them — and then address each one with the right structure.

Most couples who go through this process find it clarifying rather than confronting. The numbers become visible. The leaks have names. And the gap between what you earn and what you’re actually building starts to close.

The next article in this series walks through a step-by-step leakage audit you can begin today — the same process we use with clients to surface $1,000–$3,000 per month hiding in plain sight.

|

Find out what you’re losing — before next financial year. Book a complimentary 30-minute discovery call with Victor. We’ll give you an honest picture of where your leaks are likely coming from and what they’re costing you. cfvadvisory.com.au | Book a Complimentary Review No obligation. No product push. Just a clear conversation about your situation. |

ABOUT THE AUTHOR

| VICTOR IDOKO

CFA · CFP M.Com (Finance) Founder, CFV Advisory |

Victor Idoko is the founder of CFV Advisory in Australia and author of 7 Basic Wealth Strategies. With 11 years’ experience in financial planning, Victor is known for helping wealth builders and families create clear, practical structures to build, protect, and transfer wealth — without sacrificing lifestyle or relationships.

Victor holds globally recognised designations including the Chartered Financial Analyst (CFA) and Certified Financial Planner (CFP), alongside a Master of Commerce (Finance). His approach blends technical depth — strategy, tax-aware structuring, super and retirement planning, investment design — with the real-world family side of wealth, so plans don’t just look good on paper. They work in life. Follow the next articles in this series for the full framework — and when you’re ready to apply it to your own family, book a meeting with Victor at cfvadvisory.com.au |

General advice only. This article does not consider your personal objectives, financial situation, or needs. Victor Idoko is an Authorised Representative. Please read our Financial Services Guide and consider seeking personal advice before making financial decisions. © 2025 CFV Advisory Pty Ltd